June 24, 2023

May 3, 2024

ACAR Office Liaison Recognition | May 2024

May 2, 2024

Register Now to Start Your DE & I Certification – Ohio REALTORS

May 1, 2024

Reynolds Announces Housing Report Findings & Recommendations

May 1, 2024

Marijuana and Real Estate: A Budding Issue

May 1, 2024

ACAR Affiliate of the Month | May 2024

April 30, 2024

Legislative Spotlight

April 29, 2024

Cuyahoga County & Portage County Sexennial Reappraisal Process

April 23, 2024

CLASS ACTION CERTIFIED AGAINST CLEVELAND HEIGHTS’ ATTACK ON OUTSIDE OWNERSHIP

March 28, 2024

Local Agent in Charge – What does it mean?

March 20, 2024

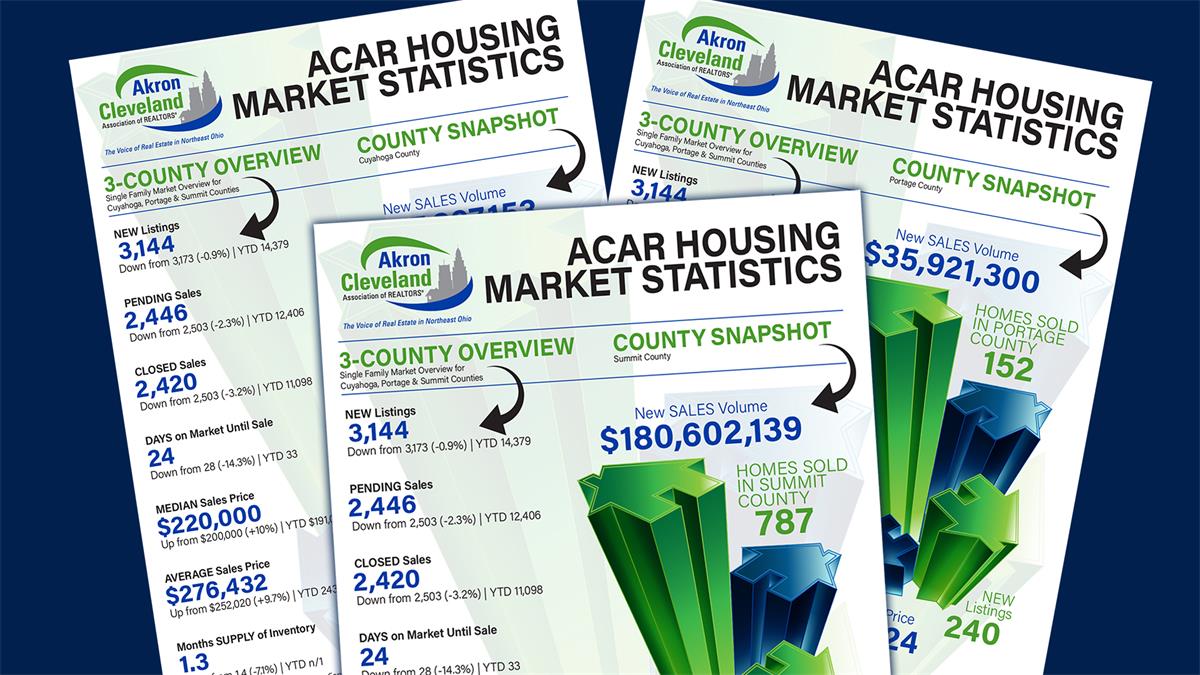

Housing Market Statistics – February 2024

February 21, 2024

Update: Cleveland Housing Overhaul Passed

February 6, 2024

Welcome to 2024 Super Diamond Elite Sponsors

Press Releases

June 10, 2021

ACAR Names Mike Valerino as New Chief Executive Officer in 2022.

April 15, 2019

Update: Real Estate Tax Relief Available to Victims of Recent Storm

March 18, 2019

Free Help for Homeowners Who are Behind on Property Taxes

February 25, 2019